Showing posts with label asset allocation. Show all posts

Showing posts with label asset allocation. Show all posts

Thursday, May 3, 2018

Wednesday, November 23, 2016

The Qualifying Charitable Distribution

Using the Qualifying Charitable Distribution (QCD) for IRA’s

There is a tax provision that allows people over 70 ½ to

transfer up to $100,000 a year from their IRA to a qualifying charity as a

direct pass-through. It usually doesn’t

affect your other taxes and can be used to satisfy your Required Minimum

Distributions. In other words – the

state and federal governments never see a dime.

I’d like to come at the opportunity from two different

angles. The first is for people who are

both generous to charity and to their family.

The second is for leaders (or soon-to-be leaders) in those charities.

For families: think of this more as succession planning than

current tax planning.

Your family inherits your assets in three buckets. Bucket one has things like real estate,

securities and personal possessions.

Your heirs may get a step-up in the cost basis so all capital gains are

forgiven. Assets pass at 100 cents on

the dollar.

Bucket two has life insurance. Structured correctly, your family gets those benefits

income tax free.

Bucket three has assets that are always taxable like

annuities and retirement accounts. If

you don’t pay the tax, your heirs will.

Your children (the employed ones) could lose up to 40% of the value to

the government.

Bucket three is the low-hanging fruit for charitable

giving. If you want to do right by your

church or cause, give them assets with limited value to your taxable heirs. Leave your family the assets they can keep. The QCD is a good start.

At your annual financial planning review, make a list of what’s

in your three buckets. You may also find

things in the first two you can do without now and enjoy the deduction. Some gifts are best given from a warm hand.

For inspiring charitable leaders: This isn’t about using the QCD – it’s about selling

it.

You know people who could contribute a lot more than they have. Next time you ask for a donation, DO NOT

ask for cash!

Try this instead:

Hello Jeff, It’s campaign time again.

Will you be using the new IRA direct transfer this year?

Huh?

It’s a loophole that allows folks to transfer money directly from their

IRA to charities like us without paying any taxes. You can use it to avoid taxes on your

required distributions too. It’s limited

to a hundred thousand dollars a year – but we can work around that. Handy estate gift too …

Er, uh ….

Why don’t you and Helen join us for lunch next Thursday? I can tell you how we’re taking advantage of

the opportunity.

See you then.

Let’s break this down:

In a few sentences, you significantly raised the bar, brought new assets

into the conversation, broached death and taxes tactfully, let him know

he’s not alone and closed for the “ask” appointment.

Does it matter if he isn’t 70 ½ yet? No.

Taking money from an IRA and deducting it works about the same as the

pass-through for most people in their sixties.

Does it matter if he doesn’t even have an IRA? No. There may be things in buckets one and

two that offer nice write-offs.

What does matter is you just started a peer-to-peer conversation

about his serious money. Cash is a byproduct

of assets. Go for the source!

BTW, big checks like this make nice challenge grants to help

other contributors find their wallets.

Leverage them. Maybe Jeff can

make a couple calls.

Your pancake breakfast isn’t going to restore the chapel. Be inspirational!

If I can help explain this to friends who serve, just say

when and where and I’ll be there.

As always, the opinions expressed here are mine and don’t

necessarily reflect the views of LPL Financial or anyone else. This is generic information so definitely run

this by your tax and legal advisors for your specific situation. They may have even better ways to have your

cake and eat it too. sh

Wednesday, July 6, 2016

On Market Timing - Part Two

“You can’t time the markets!”

Last week I shared some thoughts on why “pure” market timing

is so hard.

This week I’m going to talk about why we still include some element of market timing in regular investing.

Any attempt to diversify or allocate assets is a de facto

timing strategy. If you put more of your

money into US stocks than coffee futures, you are taking the position that: 1)

stocks could earn more than coffee, 2) stocks could earn more quickly than

coffee, or 3) stocks could earn more steadily than coffee (usually it’s #3).

We know both investments can be volatile. But we also know that they don’t always go

up or down together. By diversifying

between the two (or many more), we may reduce the chances they both go down at

the same time or speed.

Here at Helms Wealth Management, we try to own strong investments in

strong markets. But we know that we will

never have all the information. Some

choices will not succeed. The strategy

is to own an array of promising investments, so weak ones can’t derail the whole

portfolio. We always wish we had more

of the big winners- but that’s the trade-off.

I did say “promising” investments. All eligible candidates must offer the

potential to achieve your investment objectives whether they pan out or

not. Over-diversifying into every

possible investment because you don’t know which of them can help you is

expensive and frustrating.

Owning similar investment packages from multiple vendors

isn’t diversification either. The same

stock in three portfolios is still the same stock.

I believe in diversification. Most of my research time is spent trying to

find strength among asset classes, and culling the weak ones.

I’m less thrilled with static asset allocation. I’ve railed about that in most of my podcasts. If this blog hits a nerve, please have a look.

Packed asset allocation is a comprehensive investment

process that assigns pre-set mixtures of stocks, bonds, cash and other assets

based on a client’s age and risk tolerance.

The theory is that the long-term risk and return performance

of each asset has a high probability of repeating in the future. Blends of assets that produced successful

returns are offered in different volatility ranges so consumers have comfortable

choices.

The paperwork that comes with these investments clearly

states “past performance does not guarantee future results” but past performance

is better than nothing if you design an investment strategy with permanent

stock, bond, and cash ratios.

I think this takes not trying to time the markets too

far. If you aren’t a client, and you want to

know the essential portfolio management difference between Helms Wealth and many

other advisors, you just found it.

I firmly believe we should not have irrevocable faith that

investment performance will repeat. If

it doesn’t, I want a process to detect it- and I want an exit strategy for my

clients.

My favorite whipping-boy for this is the bond market.

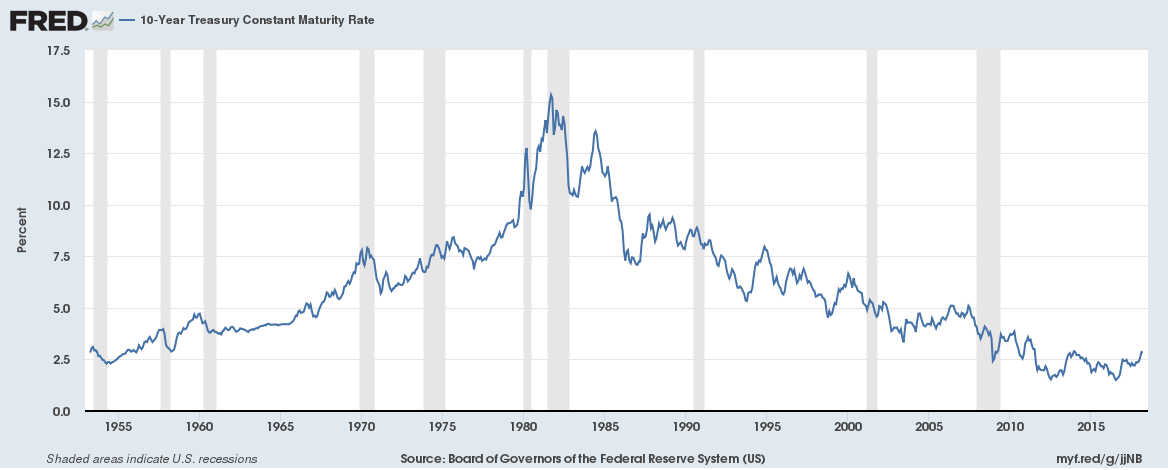

This is a chart from the Federal Reserve. It shows the yield

on 10-year US Treasury notes going back to 1953. That covers the bond market

cycle up to a few years ago.

For the first 29 years, bond values declined sharply. Falling prices drove interest rates to the

highest they have ever been in our country.

If you tried to get a mortgage in 1980 you know what I’m talking about.

From 1982 until now, bond prices have steadily appreciated

causing yields to go as low as they have ever been.

Wall Street (bless their hearts) considers a full market

cycle at between 20 and 30 years.[1] Using that methodology, they only count the

extraordinarily good half of this chart when designing ready-made investment

strategies. They can’t change it. More correctly, they haven’t yet.

When I stare at this chart, I can’t get past the fact that

we are below where the last 29-year bear market started.

Next week I’ll wrap-up by explaining what I think you need

to do about this.

Thanks for reading!

Call if you need more details, SH

The opinions expressed here are those of Skip Helms and do not necessarily reflect those of LPL Financial or anyone else. It is not possible to determine the top or the bottom of the market. Investing involves risks, including the loss of principal. Past performance does not guarantee future results. Please consider potential transactions carefully and read all appropriate materials before investing or sending money. No strategy, such as asset allocation or diversification assures a profit or protects against loss. Securities and advisory services offered through LPL Financial, a registered investment advisor. Member FINRA / SIPC

Call if you need more details, SH

The opinions expressed here are those of Skip Helms and do not necessarily reflect those of LPL Financial or anyone else. It is not possible to determine the top or the bottom of the market. Investing involves risks, including the loss of principal. Past performance does not guarantee future results. Please consider potential transactions carefully and read all appropriate materials before investing or sending money. No strategy, such as asset allocation or diversification assures a profit or protects against loss. Securities and advisory services offered through LPL Financial, a registered investment advisor. Member FINRA / SIPC

Subscribe to:

Posts (Atom)