Showing posts with label how bonds work. Show all posts

Showing posts with label how bonds work. Show all posts

Thursday, May 3, 2018

Tuesday, September 6, 2016

Visit to OLLI - Part 1

On August 5th I had the pleasure of visiting the

investment Special Interest Group of OLLI at UNC Asheville. The Osher Lifelong Learning Institute is a

program for “experienced” people to continue their education. This was my third visit and I hope they want

me back.

After the meeting, I was asked to clarify a couple of the

things I said. I think I did a better

job the second time and I’m going to expand on those answers for the next two

blogs. If you happened to be there, I hope you’ll

share these with the group since I’m not sure if the folks who asked the

questions are on the blog list.

The first question was about the relationship between bond

prices and yields.

I’ve always made a mess of trying to connect all the moving

parts conceptually but I wrote a blog last year with a practical example that

does a credible job. If you will click here for

the backstory, I’ll add some practical context.

My example was very bearish.

For the last 34 years, the bond market has been in a strong bull market.[i] Rising bond prices have dropped yields from

all-time US highs to all-time world-wide lows.

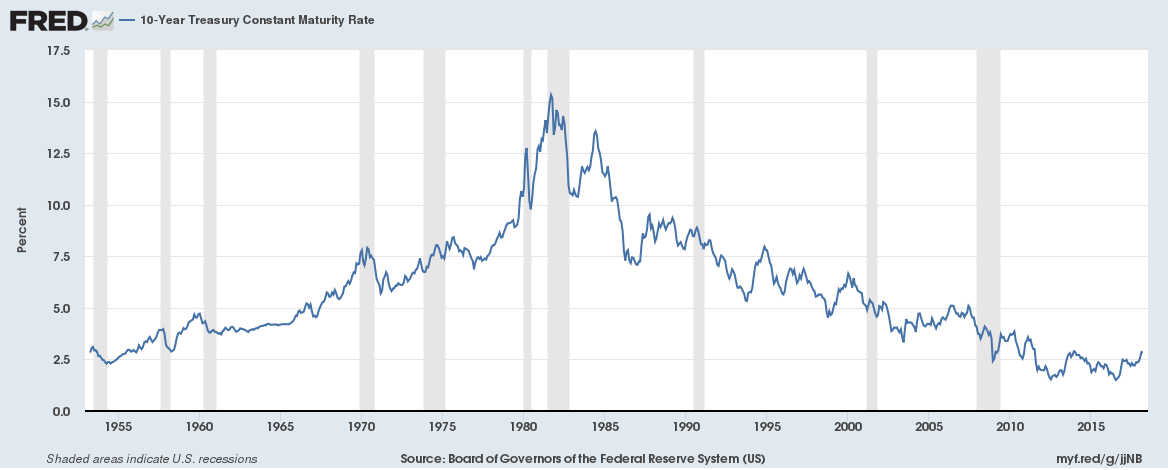

This is a chart from the US Federal Reserve showing the

yields on the US 10-year Treasury note going back to 1981. They peaked at 16% and closed last week at

1.59%.

When I talk to bond investors, they don’t always realize

that individual bonds only ever pay as much as their scheduled interest and

maturity payments. Rising prices only

affect when you enjoy the benefits.

Gains you book over the life of the investment are actually prepaid

interest you won’t see in the future. New

buyers and reinvested dividends buy new bonds at higher prices but you have to

split the lower income more ways.

Last year I shared my concern with the way my industry

markets, manages and enforces inflexible asset-allocation models. By that I mean portfolios with preset

percentages of stocks, bonds and cash.

Some of them periodically rebalance to those ratios while other follow a

“glide-path” and automatically increase fixed-income holdings as the owner gets

older.

If you’ll take a quick peek at the opening chart on my target-date podcast, you can see that by retirement, this version has roughly 2/3 of

the portfolio in either bonds or cash. Most

of these allocation models were adopted 10 to 15 years ago. Rates were a lot higher then. Once the prospectus is printed, the asset mix

is set.

This is where I think investors need to be smart. Asset allocation modeling is the industry-standard

for the retail investment business. Tens

of trillions of dollars are managed on some version of that glide-path. Years ago, managers bet the farm that those income

projections would hover around historical averages.

They didn’t.

The market meltdown drove rates lower than they have ever

been. It would take a crippling bear

market like in my example to drive them up to anywhere near those levels again.

Admitting this would be a disaster for the industry. For 25 years, the business has told investors

those allocations were sacred – that they must buy-and-hold through all market

conditions to benefit from the long-term trends.

Who’s going to tell millions of retirees they might run out

of money? Who’s going to tell them and

millions more 401(k) participants they have to reallocate to more volatile

holdings?

Nobody. Better to

keep getting paid and let customers figure that out for themselves.

Calm down. This is

good news.

If you are a long-term bond owner, you’ve already gotten

most of the income you ever will as appreciation. Bonds are still at all-time high prices. Let the next guy keep your 1.59% along with

the potential volatility of rising yields.

If they rise, you will be adding more volatility anyway so do it in

something with more upside potential.

Here’s a little homework to see if you are on a glide-path

that isn’t going where you want:

1) Open

your statement and calculate the percentage of your portfolio in bonds and

money-markets. Is it close to your

age? Double-check it on the glide-path

chart.

2) Divide

the current income those investments produce by the value of the

investments. Is that percentage enough

to cover inflation, taxes and spending money?

3) Then

tally what percentage of your portfolio can’t reasonably support your lifestyle

anymore. Who came up with that idea?

Next week I’ll take a stab at a deeper question. See you then, sh

The opinions expressed here are those of Skip Helms and do not

necessarily reflect those of LPL Financial or anyone else. Investing involves

risks, including the loss of principal. Past performance does not guarantee

future results. Please consider potential transactions carefully and read all

appropriate materials before investing or sending money. Bonds are subject to

market and interest rate risk of sold prior to maturity. Bond values will

decline as interest rates rise and bonds are subject to availability and change

in price. Rebalancing a portfolio may cause investors to incur tax liabilities

and/or transaction costs and does not assure a profit or protect against a

loss. Securities offered through LPL Financial, Member FINRA/SIPC. OLLI, Helms

Wealth Management, and LPL Financial are separate entities.

Friday, October 9, 2015

A Question on Bonds and Rates

Hello Mr. Helms,

On your podcast you said that bonds lose money when interest rates rise. I thought bonds always paid the same interest. How does that change?

You're right about the interest. The vast majority of bonds pay a fixed cash-flow during their life and return a fixed amount at maturity. Since those two things don't change, the only way markets can react to supply and demand for those payments is the price of the bond itself.

I've never done a good job explaining this. Rates and prices work inversely. It's like trying to cut your hair in the mirror.

But I've got a good example that seems to work:

Let's say you loan me $1,000. I agree to pay the owner $50 a year for the next 10 years and return the principal with the last payment -- basically a 10-year 5% bond.

A year later, you need to sell your bond. Unfortunately, the going rate for 9-year bonds has gone from $50 a year (5%) to $100 a year (10%). Nobody is going to pay you $1,000 for your bond when they can get twice the income for the same investment.

If you want to sell, you'll have to discount the price until the combination of the profit the new buyer makes in 9 years -- plus my $50 a year -- equals a 10% return. In the business that's called yield-to-maturity. Some of it is interest. Some is the gain (or loss) at payoff.

With a bond-price calculator I entered $50 a year for 9 years with $1,000 at the end at a yield-to-maturity of 10% and got a price of $712 for your bond. If rates had gone down, you could expect a profit instead.

And it isn't just your bond. Bonds are priced constantly in world markets whether they are for sale or not. That's why the values can change on your statement even with no activity.

As a rule, the longer an owner has to wait for his principal, the wider the price fluctuations because of market uncertainty. Lower-quality bonds usually fluctuate more than high-quality bonds for the same reason.

So the best answer to your question is that yields rise because bond prices fall. The new owner's increased yield comes from the old owner's wallet.

I used an extreme example to show the process. Rates doubling in a single year would be a disaster for the bond market and probably every other financial market in the bargain. Right now rates are historically low but don't appear to be in any hurry to go up either.

And advisors can't legally borrow money from clients. -SH

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

Subscribe to:

Posts (Atom)